Performance, Regulation, and Investment Dynamics

Introduction

Africa’s minerals sector is at a structural inflection point. The continent is no longer defined only by resource abundance, but by how regulation, foreign direct investment (FDI), and trading systems are shaping global supply chains. From cobalt and copper powering electrification to iron ore reshaping steel markets, Africa’s minerals are increasingly governed by policy‑driven market design, not just commodity cycles.

—

Africa’s Global Mineral Position (Overview)

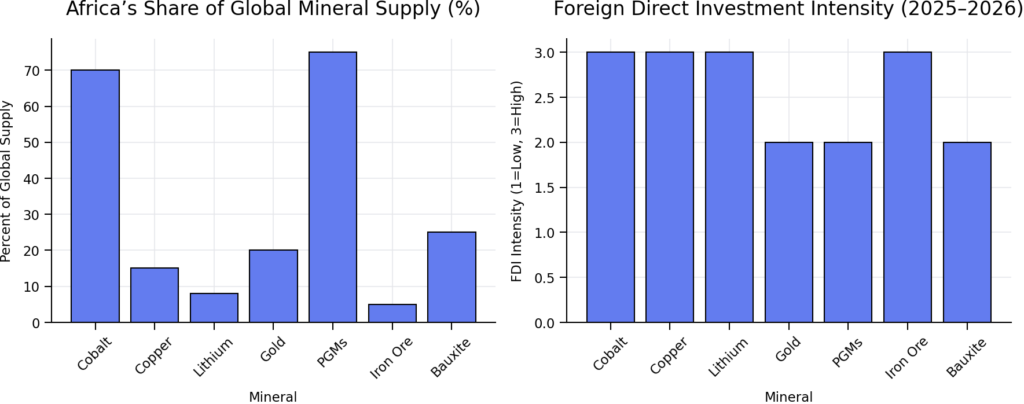

The chart below highlights Africa’s approximate share of global supply for its most strategic minerals.

Key insight: Africa holds dominant or structurally significant shares in cobalt, platinum group metals (PGMs), bauxite, and gold—giving governments growing leverage over global industrial systems.

—

Cobalt – Strategic Control Through Regulation (DRC)

Africa—via the Democratic Republic of Congo—supplies roughly 70% of global cobalt, making it indispensable for EV and battery value chains.

2026 performance outlook

Production remains strong, but pricing is moderated by export quotas and state oversight rather than market cycles.

Regulation and trading developments

The DRC has shifted from export bans to quota‑based exports, reinforcing state control over volumes and timing. Cobalt trading is increasingly contract‑based, with long‑term offtake agreements replacing spot markets.

FDI trend

Investment remains high, dominated by Chinese firms, while U.S.‑ and EU‑backed players are re‑entering via exploration and logistics corridors.

—

Copper – Africa’s Strongest Structural Performer (Zambia & DRC)

Copper underpins electrification, renewable energy, and data infrastructure, making it one of Africa’s most valuable growth minerals.

2026 performance outlook

Firm prices and rising output position copper as Africa’s best‑performing mineral structurally, rather than cyclically.

Regulation and trading developments

Zambia’s sliding royalty regime has restored fiscal predictability, while the DRC maintains open exports. Trading is increasingly linked to infrastructure corridors rather than open spot markets.

FDI trend

Large‑scale reinvestment by global miners and Gulf‑linked financiers is focused on mine‑plus‑infrastructure models.

—

Lithium – Strategic, Volatile, and Policy‑Driven (Zimbabwe, Namibia, DRC)

Africa’s lithium sector has moved rapidly from exploration to early production.

2026 performance outlook

Strategically critical, but margins are under pressure due to global oversupply.

Regulation and trading developments

Zimbabwe has introduced export quotas and processing mandates, with a full ban on unprocessed exports from 2027. Trading is shifting toward processed intermediates and long‑term supply contracts.

FDI trend

Chinese investment dominates, while European partners seek upstream security for EV supply chains.

—

Gold – Africa’s Financial Anchor

Gold remains Africa’s most reliable cash‑flow mineral.

2026 performance outlook

High global prices support near‑record profitability despite rising costs.

Regulation and trading developments

Export regimes remain open and stable. Trading increasingly involves central banks and sovereign buyers.

FDI trend

Sustained investment from Canadian, Australian, and Gulf‑based firms reflects gold’s low regulatory risk profile.

—

Platinum Group Metals – Optionality for the Energy Transition (South Africa)

Africa dominates global supply of platinum and related metals.

2026 performance outlook

Selective recovery led by platinum, with hydrogen technologies providing long‑term upside.

Regulation and trading developments

South Africa’s Mining Charter obligations are increasingly embedded in law, prioritizing transformation and community benefits.

FDI trend

Capital is focused on efficiency upgrades and ESG‑aligned downstream applications rather than greenfield expansion.

—

Iron Ore – Structural Disruption from Simandou (Guinea)

Guinea’s Simandou project is redefining global iron ore supply.

2026 performance outlook

The impact is structural, not cyclical, as high‑grade ore enters the market.

Regulation and trading developments

State‑regulated rail and port systems limit open trading but enhance long‑term reliability.

FDI trend

Over US$20 billion in foreign investment has been committed to Simandou and its infrastructure.

—

Bauxite – Stable Volumes, Strategic Importance (Guinea)

Guinea controls over a quarter of global bauxite reserves.

2026 performance outlook

Stable production and modest price growth.

Regulation and trading developments

Mining licenses are increasingly tied to rail and port investments.

FDI trend

Chinese dominance continues, with rising Gulf interest in alumina processing.

Conclusion

In 2026, Africa’s mineral markets are no longer defined solely by geology or commodity cycles. Export quotas, beneficiation mandates, and state‑controlled logistics have become market‑shaping tools. The continent’s minerals sector has entered a strategic phase where regulation, infrastructure, and geopolitics directly influence global supply chains.

Africa’s minerals are not just resources—they are instruments of economic and geopolitical leverage.